HKU Jockey Club Enterprise Sustainability Global Research Institute

World-Class Hub for Sustainability

Zhan Shi | Shaojun Zhang

Beyond Brown: Oil Shocks and Carbon Premium

July 15 2026

Key Takeaways

- Research Question: Does the carbon premium isolate financial markets’ pricing of carbon-transition risk, or does it also reflect oil shocks transmitted through oil-dependent extractive firms inside brown portfolios?

- Data: The paper links S&P Trucost firm-level carbon-intensity data to U.S. corporate bonds and equities from October 2003 to December 2022. It measures cost of capital using option-adjusted corporate bond yield spreads, option-implied expected equity returns, and analyst-forecast-based implied cost of capital.

- Method: The empirical design combines portfolio decomposition, firm-level panel regressions, daily event studies, Paris Agreement re-examination, structural oil-shock decomposition, renewable-energy falsification tests, and historical evidence from 1974 onward.

- Findings:

- Brown portfolios combine firms with different economic exposure to oil. Energy firms account for about 25% of brown bonds and 18% of brown equity, even though their average carbon intensity is lower than that of Utilities and Materials.

- Oil shocks operate mainly through the oil premium, defined as the cost-of-capital spread between upstream extractive firms and other brown firms. These shocks have no stable effect on the non-energy carbon premium.

- The post-Paris Agreement increase in the bond carbon premium is largely explained by the 2014–2016 oil-price collapse. After separating upstream extractive firms or adding sector-by-time fixed effects, the aggregate Paris Agreement effect largely disappears.

- Implications: Climate-finance research and sustainable investment practice should distinguish commodity-cycle exposure from carbon-transition exposure before interpreting brown-green spreads as evidence of market discipline against emissions.

Source Publication:

Shi, Zhan, and Shaojun Zhang. 2026. “Beyond Brown: Oil Shocks and Carbon Premium.” SSRN Working Paper, February 2026.

Background and Motivation

What finance calls a carbon penalty may be little more than an oil-price cycle with better branding.

A central premise in climate finance is that capital markets can price the low-carbon transition before policy fully arrives. If investors require higher returns from high-emission firms, financing costs can become part of the transition mechanism, redirecting capital away from carbon-intensive production. The carbon premium offers a direct way to test this premise: it compares the cost of capital of brown firms with that of green firms.

The measure is influential because it is simple. That simplicity is also its main empirical risk. A brown portfolio can include a regulated utility, a materials producer, and an oil-and-gas firm, even though these firms face different cash-flow exposures when oil prices move. In our paper, we ask whether the observed carbon premium captures a market-wide price of transition risk, or whether part of the premium is an oil-cycle statistic embedded in a carbon-sorted portfolio.

A Premium Built on Crude

The first finding is compositional. Brown portfolios are dominated by Utilities, Materials, and Energy, but these industries are economically different. Utilities carry the highest average carbon intensity by a wide margin, yet the oil-dependent upstream extractive firms (also known as hard commodity firms, e.g., Energy and Metals & Mining) account for about 30% of brown bonds and 21% of brown equity, among the largest weights in carbon-sorted portfolios.

For these upstream extractive firms, oil prices determine their output values and growth options, and higher oil prices reduce their value betas and required returns. For downstream brown firms such as utilities, oil is mainly an input cost; in competitive markets they can often pass much of the shock through to output prices, leaving a smaller net effect on margins. An oil-price move therefore shifts extractive firms sharply while leaving other brown firms largely unaffected.

The Paris Agreement in December 2015 is the paper’s main identification setting—and the most studied event in climate finance. Standard event-study specifications find that the equity and bond carbon premium increased by about 1.2 percentage points and 34 basis points after December 2015, respectively, which is often read as evidence that markets began pricing transition risk after a landmark climate-policy event.

The timing tells a different story. The estimated carbon premium had already been rising for roughly 18 months before Paris. By mid-2015, the U.S. energy sector was in mounting financial distress amid the oil-price collapse, with 42 exploration and production firms filing for bankruptcy that year. The Paris Agreement arrived near the trough of an oil-market crash that had already altered extractive firms’ financing conditions. Furthermore, OPEC’s 168th meeting—when Iran refused to freeze output in anticipation of sanctions lifting—came just days before the Agreement was adopted on December 12.

We examine three episodes of confounding oil shocks from 2014 to 2016 using daily event studies: OPEC’s November 2014 price war decision, the mid-2015 Grexit referendum and China growth scare, and the November 2015 dollar appreciation following Fed Chair Yellen’s testimony. In each episode, extractive firms’ expected equity returns and bond yield spreads move sharply on news days. Broad brown firms do not experience incremental response once these oil-dependent firms are controlled.

This pattern applies to the overall Paris effect. Once upstream extractive firms are separated from other brown firms, the post-Paris increase for downstream brown firms falls from about 1.2 percentage points to an insignificant level in equity and from 34 basis points to 6 basis points in bonds. Repricing is concentrated among extractive firms, whose cost of equity capital increases by almost 5 percentage points and whose cost of debt rises by more than 100 basis points.

Daily analysis points the same way. Carbon-premium movements line up with oil-market news days, not climate-policy news days or other days; once oil-news-driven price dynamics are accounted for, the standard post-Paris carbon premium largely disappears.

The general evidence supports the oil-channel interpretation. Over the 2003–2022 sample, plausibly non-climate oil shocks move extractive firms’ financing costs sharply—higher oil prices lower their required returns, and oil-price declines raise them—while downstream brown firms show much weaker, mixed responses. A renewable-energy falsification test supports the interpretation: when oil prices fall, renewable firms’ financing costs rise alongside extractive firms, consistent with an energy-market channel rather than a brown-to-green reallocation.

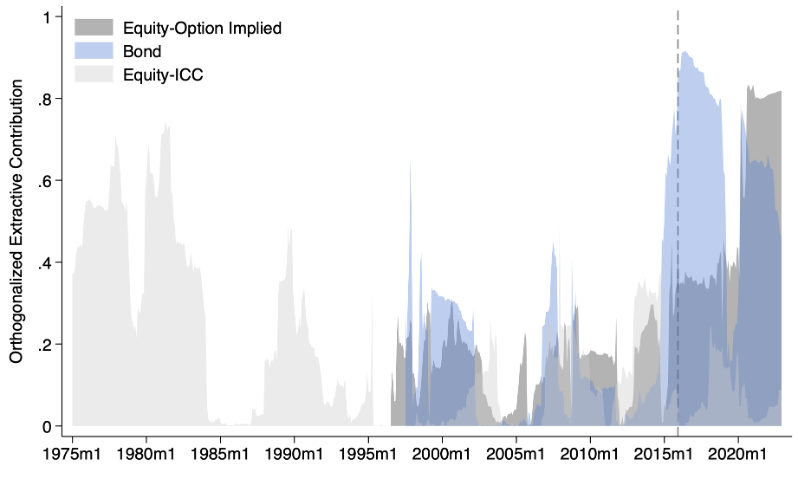

Historical evidence reinforces this. The negative relation between oil prices and oil-dependent firms appears in data going back to 1974, well before climate transition risk entered the financial mainstream. Energy-specific movements explain a large share of aggregate carbon-premium variation across every major oil disruption of the past five decades, from the 1980s oil glut through the Global Financial Crisis, the 2014–2016 crash, COVID-19, and the 2022 Russo-Ukrainian war.

Figure 1: Contribution of Oil-Specific Dynamics to Carbon Premium Variation

Reading the Signal Wrong

These findings challenge how the carbon premium should be interpreted. A higher brown-green spread during an oil shock is not sufficient evidence that markets are pricing carbon-transition risk. It may reflect the financing conditions of energy firms whose cash flows and risk exposures move with the oil cycle.

For investors, this is a risk-attribution problem. Carbon-sorted portfolios can mix transition-risk exposure with commodity-cycle exposure. Strategies that treat the aggregate carbon premium as a clean climate signal may overstate the extent to which markets penalize high-emission production.

For policymakers, the findings caution against reading aggregate carbon-premium movements as evidence that financial markets are already disciplining emissions. During major oil shocks, the apparent carbon signal may say more about energy-sector fundamentals than about expectations of future climate policy.

Zhan Shi is an Associate Professor at PBC School of Finance, Tsinghua University.

Shaojun Zhang is an Associate Professor of Finance at the Ohio State University, Fisher School of Business.