HKU Jockey Club Enterprise Sustainability Global Research Institute

World-Class Hub for Sustainability

Hanwen Sun | Bohui Zhang | Yue Zhang

Anti-ESG Policy Spillovers: Evidence from U.S. Public Pension Funds

May 29, 2026

Key Takeaways

- Research Question: Do state-level anti-ESG laws in the U.S. generate cross-state spillovers in corporate ESG performance through public pension fund ownership networks?

- Data and Method: The study employs a staggered difference-in-differences (DiD) design using the state-level anti-ESG bills, equity holdings from major state pension funds, and ESG outcomes for public firms from 2018–2023.

- Findings:

- Firms with greater exposure to pensions subject to anti-ESG mandates experience significant declines in ESG performance, equivalent to 2.5%–3% of the cross-sectional standard deviation.

- Spillovers operate through both active portfolio reallocation away from ESG-intensive firms and the withdrawal of environmental and social shareholder engagement.

- The effects are politically contingent, with ESG declines concentrated among firms headquartered in Republican-leaning states, whereas firms in Democratic-leaning states are relatively insulated.

- Markets respond asymmetrically: low-ESG firms earn positive abnormal returns around bill enactment, and exposed firms show modest improvements in accounting profitability.

- Implication: State-level political constraints on institutional investors can transmit through ownership networks, weakening corporate sustainability and generating economy-wide externalities beyond enacting jurisdictions.

Source Publication:

Sun, H., Zhang, B., and Zhang, Y. (2026). “Anti-ESG Policy Spillovers: Evidence from U.S. Public Pension Funds,” SSRN Working Paper.

Background and Research Focus

Since 2021, the U.S. has witnessed a rapid politicization of sustainable investing, with a growing number of states enacting legislation that restricts public pension funds from incorporating environmental, social, and governance considerations into investment decisions. Framed around “pecuniary-only” fiduciary standards, these laws prohibit the consideration of ESG factors unless they are deemed strictly material to financial returns.

Although the immediate targets of these statutes are state-affiliated investors, public pension funds are among the largest and most geographically diversified institutional owners in U.S. equity markets. This finding raises a fundamental question with national relevance: Can state-level political interventions propagate beyond their jurisdictions by reshaping the behavior of firms headquartered elsewhere? The study addresses this question by examining whether anti-ESG mandates generate spillover effects on corporate sustainability outcomes through pension fund ownership networks.

Data and Empirical Strategy

The authors construct a comprehensive dataset covering 182 anti-ESG bills introduced across 36 states between 2021 and 2023, of which 30 laws enacted in 16 states directly restrict public pension investment practices. These legislative events are matched with quarterly Form 13F filings from 32 major U.S. state pension funds, which together manage approximately USD 680 billion in domestic equities and account for nearly 60% of total public pension equity holdings.

To isolate cross-state spillovers, the analysis excludes firms headquartered in the enacting states, focusing instead on 2,605 publicly listed firms observed over 11,592 firm-year observations. Firms’ exposure to anti-ESG legislation is measured by the share of their equity held by pensions subject to these mandates. The primary empirical framework is a staggered DiD design, with firm-level ESG performance measured using MSCI weighted-average ESG scores. Extensive robustness checks address pre-trends, alternative ESG measures, alternative samples, alternative model specifications, and potential confounding influences from other institutional investors.

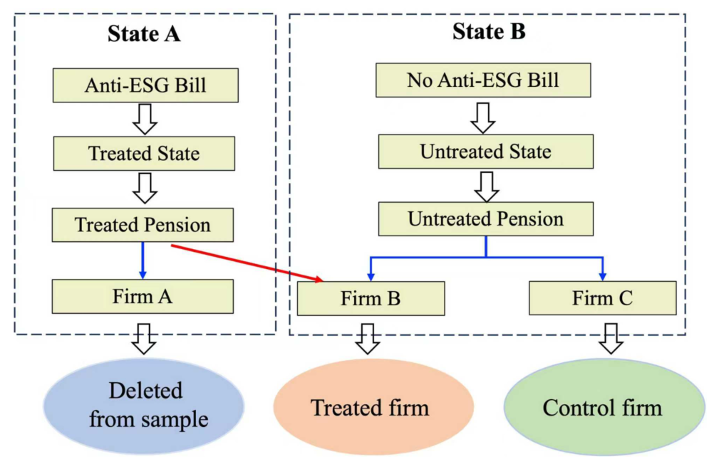

Figure 1: Sample Construction and Treatment Identification

Note: This figure illustrates how firms are classified based on state-level anti-ESG legislation and pension fund exposures. In State A, which passes an anti-ESG bill, the state pension is classified as a treated pension. Firms directly headquartered in the treated state (e.g., Firm A) are removed from the sample to avoid confounding effects. However, if the treated pension invests in firms located in other states (e.g., Firm B in State B), those firms are designated as treated firms. By contrast, firms not connected to treated pensions (e.g., Firm C in State B) serve as control firms.

Findings and Interpretation

The results show firms with greater exposure to pensions constrained by anti-ESG legislation experience a persistent decline in ESG performance following bill enactment. Dynamic estimates confirm these effects emerge after legislation takes effect and do not reflect differential pre-treatment trends, indicating a causal ownership-based channel rather than coincidental regulatory timing.

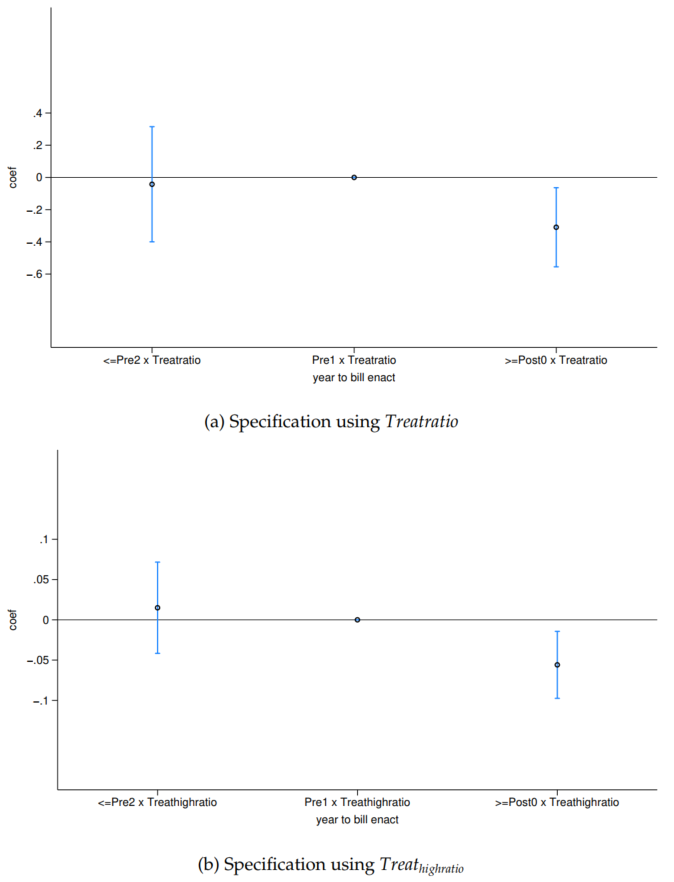

Figure 2: Pre-trend Analyses

Note: This figure assesses the parallel-trends assumption prior to the enactment of anti-ESG legislation. Panel (a) plots estimated coefficients from a specification using the continuous treatment measure (Treatratio), interacted with event-time indicators. Panel (b) shows results based on the binary treatment classification (Treathighratio). The vertical axis displays coefficient estimates, and the horizontal axis indicates event time relative to the bill enactment year. Because the estimation is based on a balanced window spanning the pre- and post-bill periods, and the duration of the pre- and post-bill periods varies across firms, we focus on the cumulative effects during these periods. ≤ Pre2 refers to the period two years prior to the bill passage, and ≥ Post0 denotes the years following the bill’s passage. When the dynamic effect is not cumulative, the plots also indicate parallel trends during the pre-bill period, which are available upon request.

Two mechanisms jointly explain these spillovers. First, along the exit channel, treated pension funds actively rebalance their portfolios away from ESG-intensive firms. Decomposition of portfolio weight changes demonstrates these shifts are driven by discretionary trading decisions rather than passive price movements, with ownership reductions occurring rapidly within three quarters of bill passage. Second, along the voice channel, anti-ESG mandates sharply curtail stewardship activity. Exposed firms receive fewer environmental and social shareholder proposals, proposal success rates decline, and treated pensions effectively withdraw from ESG-related agenda setting altogether. Notably, these effects are concentrated in the environmental and social dimensions, with governance practices largely unaffected.

The magnitude of the spillovers is strongly conditioned by local political context. Firms headquartered in Republican-leaning states exhibit pronounced ESG declines, whereas firms in Democratic-leaning states appear more resilient, suggesting supportive local institutions or countervailing stakeholder pressures can partially offset the withdrawal of ESG-oriented institutional ownership.

Financial markets appear to internalize these shifts. Low-ESG firms earn positive abnormal returns around the announcement of anti-ESG laws, whereas firms with high exposure to treated pensions subsequently show modest improvements in accounting performance, including return on assets and return on equity. These patterns are consistent with firms scaling back ESG-related investments and compliance efforts in response to reduced investor pressure.

Implications

The study highlights the systemic role of public pension funds as conduits through which political and ideological mandates shape corporate behavior. By constraining both capital allocation and shareholder engagement, anti-ESG legislation weakens a key institutional mechanism supporting corporate sustainability, even in states that have not enacted such laws. More broadly, the findings underscore how fragmented political interventions in financial markets can propagate through ownership networks, complicating efforts to sustain coherent and stable ESG practices at the national level.