HKU Jockey Club Enterprise Sustainability Global Research Institute

World-Class Hub for Sustainability

HomeHKU Sustainability IndexFirm-level Climate Change Expo...

Firm-level Climate Change Exposure Index

Firm-level Climate Change Exposure Index

Objectives

A new methodology for quantifying firm-level climate change exposure from earnings conference calls. The index captures attention paid by managers and financial analysts to climate topics. The measures, available for over 10,000 firms across 34 countries from 2002 to 2023, are useful in predicting important real outcomes related to the net-zero transition, notably job creation in disruptive green technologies and green patenting, and they contain information that is priced in options and equity markets.

Key Innovation

- • Instead of relying on traditional methods, the researchers analyze earnings call transcripts to provides a valuable tool for researchers and investors to assess firm-level climate change risk and opportunities.

- • Highlights the heterogeneous impacts of climate change, even within industries.

- • Offers insights into how firms are responding to climate change, through innovation and investment.

Methodology

A machine learning keyword discovery algorithm has been adopted to capture exposures related to climate change opportunities, physical risks, and regulatory risks.

Bigram Construction: The algorithm starts with a short list of initial keywords to identify climate change-related “bigrams” (pairs of words) in earnings call transcripts. It then discovers new climate change bigrams by reverse-engineering a machine-learning process.

The bigrams are categorized into:

- • Overall climate change exposure.

• Opportunities arising from climate change (e.g., renewable energy).

• Physical risks associated with climate change (e.g., sea-level rise).

• Regulatory risks (e.g., carbon taxes).

- • Overall climate change exposure.

The frequency of these bigrams, scaled by the total number of bigrams in the transcript, is used as a firm-level measure of climate change exposure.

Sentiment and Risk Measures: The researchers also construct “sentiment” measures (positive or negative tone) and “risk” measures (frequency of climate change bigrams mentioned with “risk,” “uncertainty,” or synonyms).

TF-IDF Adjustment: Term Frequency-Inverse Document Frequency is used to weigh bigrams according to their representativeness for climate discussions.

Regression Analysis: The paper uses various regression models (OLS, Poisson) and fixed effects to analyze the relationship between climate change exposure and real/financial outcomes.

Variables and Formats

The variable names consist of three parts.

- The first part refers to general climate change as well as three topics related with climate change: opportunity, physical, and regulatory. They are ‘cc’, ‘op’, ‘ph’ and ‘rg’.

- The second part refers to different metrics. We have exposures (‘expo’), risks (risk), positive sentiment (‘pos’), negative sentiment (‘neg’), and overall sentiments (‘sent’).

- The third part refers to the weighting scheme of climate change bigrams. Equal weighted scores are denoted by ‘ew’, and TFIDF weighted scores are denoted by ‘tfidf’ (available for legacy data only).

Please refer to the document before using the data. These details are critically important to ensure proper usage.

Findings & Results

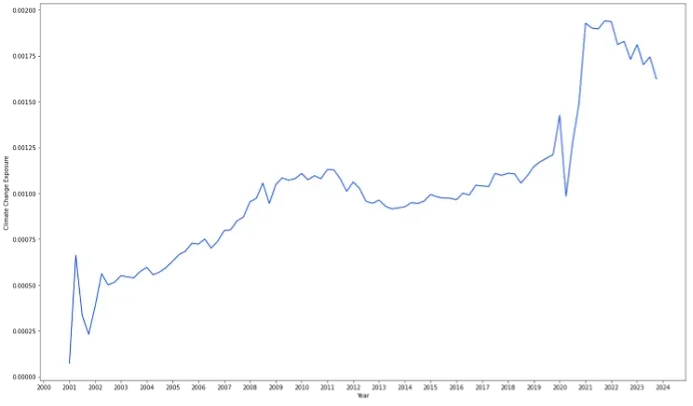

Figure 1 Climate Change Exposure (CCE) rockets in 2021 and then cools down

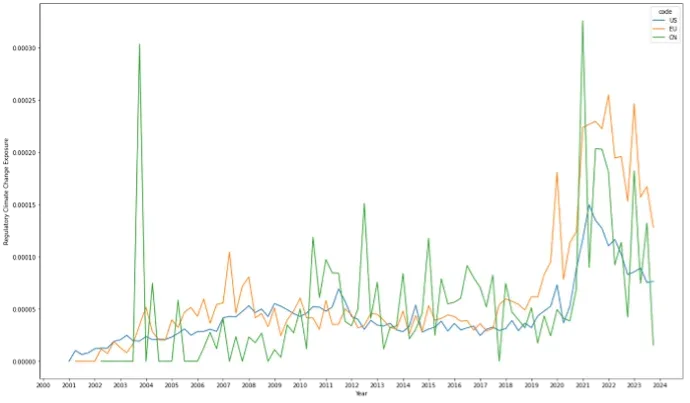

Figure 2 Europe leads Regulatory CCE in recent years

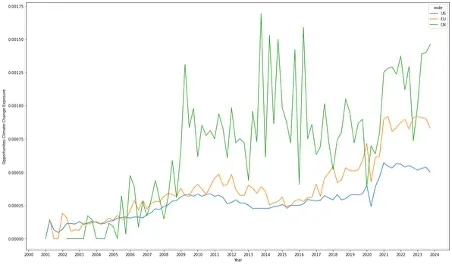

Figure 3 China Opportunity CCE leads US / Europe

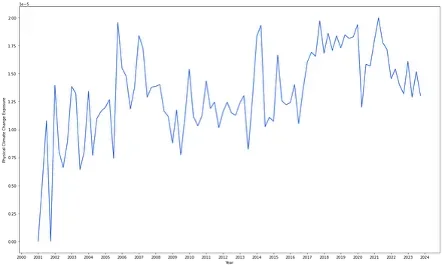

Figure 4 Physical CCE remains volatile

Coverage

10,000 firms across 34 countries when the firms’ earnings call transcripts are available.

Update Frequency

Annually

Papers that Develop and Use these data

Sautner, Z., Van Lent, L., Vilkov, G., & Zhang, R. (2023). Firm‐level climate change exposure. The Journal of Finance, 78(3), 1449-1498.