HKU Jockey Club Enterprise Sustainability Global Research Institute

World-Class Hub for Sustainability

Marc Goergen | Luc Renneboog | Yang Zhao

Insider Trading in Connected Firms during Trading Bans

Apr 1, 2025

Key Takeaways

- The study investigates whether corporate insiders, particularly “connected directors” serving on multiple boards, exploit insider information during trading bans (close periods) by trading in the stocks of connected firms not subject to the ban.

- Directors are more likely to trade in their connected firms when they are prohibited from trading in a close period in one of their firms.

- The direction of trading in connected firms (buy/sell) is influenced by whether the insider information about the firm subject to a close period is positive or negative.

- T positive correlation exists between the market reactions (CARs) in the firms subject to close periods and the connected firms where trading occurs.

- This positive correlation is more pronounced when the connected firms have friendly relationships, such as being partners or operating in highly concentrated industries.

- The positive correlation is also stronger when the connected firms have high levels of institutional ownership. This finding suggests institutional investors monitor the trading activities of connected directors.

- Regulators may need to extend trading bans to all firms where a director holds board seats to prevent insiders from circumventing trading restrictions.

Source Publication:

Marc Goergen, Luc Renneboog, Yang Zhao. (2025). Insider Trading in Connected Firms during Trading Bans. HKU Jockey Club Enterprise Sustainability Global Research Institute Working Paper No. 2025/004.

Background and Research Questions

Corporate insiders can often earn abnormal returns when trading their firms’ shares, due to their informational advantage. To restrict this advantage, regulators impose trading bans (called “close periods” in the UK) before the release of significant information such as earnings announcements. Although insiders cannot trade shares of their own firm during these periods, those holding multiple directorships can trade in their other firms. Moving beyond the traditional focus on within-firm insider trading patterns, this research uniquely examines cross-firm information exploitation and explores three questions: Do directors with multiple board seats trade more in their connected firms during close periods? Is this trading influenced by information from the firm under a close period? Do investors use information from these trades to trade in the firms under close periods?

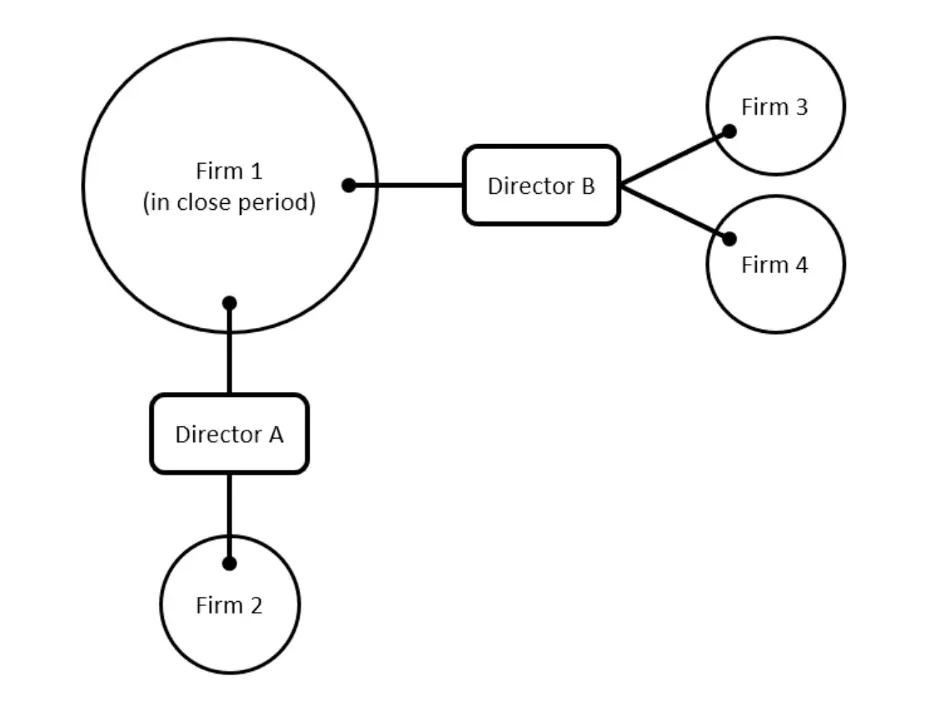

Figure 1: Connected Directors and Connected Firms

Director A sits on the boards of firms 1 and 2. Director B sits on the boards of firms 1, 3, and 4. Firm 1 is subject to a close period.

Data and Methodology

The researchers analyzed 86,258 insider transactions on the London Stock Exchange between 1999 and 2019. Among these, 40.7% (35,109) were executed by connected directors holding multiple board positions. Notably, 21% (7,384) of these connected-director transactions occurred while the director faced a close period in at least one of their other firms.

The study measured market reactions using cumulative abnormal returns (CARs) around insider transaction announcement dates. For firms under close periods, CARs were computed over the same event windows as the traded connected firms. To establish causality and rule out market-wide trends as an alternative explanation, the researchers also conducted placebo tests with random pairs of unconnected firms.

To investigate moderating factors, the study classified firm relationships using two measures: (1) identifying “Partner” relationships through FactSet data, and (2) calculating sector concentration using the Herfindahl–Hirschman Index (HHI), with firms in sectors with HHI in the top tercile classified as having potentially friendly relationships.

To control for potential confounding events, the researchers excluded transactions concurrent with major corporate announcements such as mergers, acquisitions, and CEO changes. This approach ensured the observed market reactions were attributable to insider trading information rather than other significant events.

The institutional ownership analysis segmented firms based on their institutional investor presence, examining how the level of institutional ownership influenced the correlation between CARs in connected firms.

The study employed logistic and OLS regressions to analyze trading patterns.

Findings and Discussion

The analysis revealed several significant patterns. First, directors restricted by close periods trade more frequently in their connected firms, suggesting a strategic shift in trading activity. Second, the direction of these trades aligns with the insider information’s nature—directors buy connected-firm shares when possessing positive information about the close-period firm and sell when the information is negative.

Most importantly, the market reactions (CARs) in the traded connected firms positively correlate with those in the close-period firms across various event windows. This correlation persists after controlling for other events such as mergers or CEO changes and isn’t explained by general market momentum, as confirmed by placebo tests showing no correlation between unconnected firms.

Further analysis revealed two key moderating factors. The positive correlation strengthens when the firms have “friendly relationships” (partnerships or operations in concentrated sectors), suggesting insider information is more valuable between closely related firms. Additionally, the correlation intensifies with higher institutional ownership, indicating institutional investors monitor connected directors’ trading activities and react accordingly.

Policy or Market Implications

This study demonstrates connected directors can partially evade trading bans by exploiting insider information across their network of board positions. Although this behavior may not technically violate current regulations, it challenges the effectiveness of existing trading-ban policies.

The research has important implications for regulatory frameworks. In April 2024, the SEC’s first “shadow trading” enforcement action found Matthew Panuwat liable for purchasing stock in a competing firm, based on nonpublic information about his firm’s acquisition. This precedent, combined with the evidence from this study, suggests regulators may need to broaden the scope of close periods to include all firms where a director holds a board position.

For investors, these findings highlight the information value contained in the trading patterns of connected directors, especially during close periods, and suggest monitoring such transactions could provide valuable trading signals.